{kind=link}

Comparative snapshot

In practice, choosing between a one-off loan and an open credit line is about matching cash flow to purpose; this is where didi prestamos fits neatly into everyday decisions. The comparative logic is simple: a short-term cash need calls for a fixed loan with a clear repayment schedule, while recurring gaps suit a revolving credit facility. My tone here is descriptive — I’ll trace differences, show trade-offs, and point you to practical metrics you can use right away.

Core differences: loans versus credit

A traditional loan from DiDi Finance means a set principal, a stated loan term, and a predictable monthly payment. That predictability helps planning: you know the interest rate and the expected APR up front. The credit alternative—often labeled as “credit”—behaves more like a safety net: you draw, you repay, you draw again. Underwriting criteria can be similar, but the repayment rhythm changes. In short: loans tame volatility; credit lines absorb it.

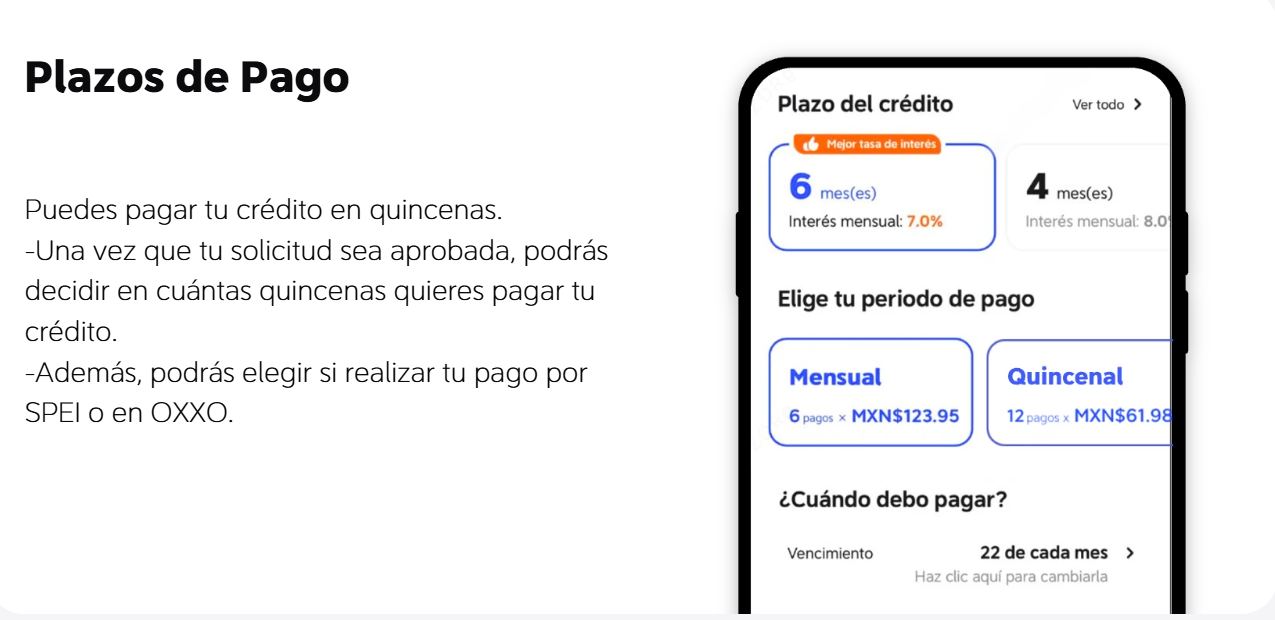

Practical features that matter

Focus on three operational features when comparing offers: interest rate, repayment schedule, and fees. Interest rate determines monthly cost; repayment schedule dictates cash-flow timing; fees—origination or late—can shift effective APR. For many users the smallest detail—an early-repayment penalty—turns a seemingly cheap loan into an expensive one. Keep these mechanics front and center when you evaluate options.

Real-world anchor: context from the streets of Mexico City

During the 2020 COVID-19 downturn, many drivers and gig workers in Mexico City turned to instant online lending to cover immediate expenses, showing how tightly cash-flow problems map to service design. That shift underlined a need for transparent products like prestamos en linea al instante, where speed and clarity are the point. This anchor matters because it reveals user behavior: when earnings dip, predictability and access matter more than headline rates.

User scenarios and common mistakes

Scenario one: a driver needs a car repair and chooses a 24-month loan for a small amount. The result is higher total interest than a shorter term would have produced. Scenario two: someone uses a credit line for everyday shortfalls and slowly accumulates a large balance—fees and compounding interest follow. The common mistakes are consistent: ignoring APR, mismatching loan term to purpose, and assuming credit lines are free. These errors cost real money—avoid them.

Comparative checklist for decision-making

Use this quick checklist when comparing DiDi Finance options: 1) match term to need (short repair → short loan), 2) calculate APR not just nominal rate, 3) verify fees and penalties. A small spreadsheet will expose the difference between two offers in minutes. Keep credit score considerations in mind—higher scores usually win better terms. —It’s not glamorous, but the arithmetic decides outcomes.

How to decide: three pragmatic rules

Base your choice on these three evaluation metrics: effective APR, total repayment amount, and flexibility (prepayment options and redraw features). Measure APR to compare across offers, total repayment to see long-term cost, and flexibility to gauge fit for unpredictable income. These are simple, measurable, and they map directly to monthly budgeting.

Advisory close: golden rules before you commit

1) Always compute APR and total repayment before signing—this reveals the true cost. 2) Match term to purpose: short emergencies need short loans; recurring shortfalls may justify a credit line but watch utilization rates. 3) Prioritize transparency: clear repayment schedules and stated fees reduce surprises and protect your monthly budget.

DiDi Finanzas offers both approaches; the value lies in picking the one whose mechanics align with your cash flow and avoiding hidden fees—simple math, honest terms. —Final thought: practical choices beat flashy offers every time.